Why CRED Gives You Rewards Just for Paying Your Bills

At first glance, CRED seems too generous.

You pay your credit card bill — something you were already going to do — and CRED gives you reward points, cashback, and exclusive deals.

Why would a company reward you for something you’d do anyway?

The answer reveals one of the smartest business strategies in modern Indian startups.

CRED Is Not a Rewards App

Most people think CRED is a rewards platform.

It isn’t.

CRED is a data company that used rewards to build the most valuable consumer database in India.

Think about what happens when you use CRED:

- You link your credit cards

- CRED sees your spending patterns

- Your income bracket becomes obvious

- Your lifestyle, habits, and financial behaviour are all visible

CRED didn’t want your bill payment. It wanted your data.

The Loss Leader Strategy

In business, a loss leader is when a company sells something at a loss — or gives it away free — to gain something more valuable in return.

Classic examples:

- Printers sold cheap → profit from ink cartridges

- Razors sold cheap → profit from blades

- Jio gave free data → built 400 million users overnight

CRED’s rewards are its loss leader. Every cashback, every reward point, every exclusive deal costs CRED money upfront.

But in return, CRED gets access to India’s most financially active, high-credit-score consumers.

That audience is worth far more than the rewards cost.

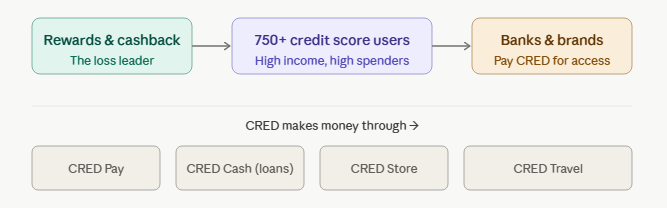

Why High Credit Score Users Specifically?

CRED only allows users with a credit score above 750.

This was not random.

People with high credit scores are:

- Higher income earners

- Financially responsible

- More likely to repay loans

- Bigger spenders on premium products

For any bank, lender, or premium brand trying to reach this audience — CRED became the perfect gateway.

That’s the real business model.

CRED charges financial institutions and premium brands to access its curated, high-quality user base.

What CRED Actually Sells

CRED makes money through:

- CRED Pay — its own payment product

- CRED Cash — personal loans to verified users

- CRED Store — premium brand partnerships

- CRED Travel — hotel and flight bookings

Notice the pattern.

Every product CRED launched targets the same high-income, financially active user — the exact person brands and lenders are desperate to reach.

The rewards were never the product.

You were always the product.

The Sunk Cost That Keeps You Hooked

Once you’ve accumulated CRED coins and rewards, leaving feels like a loss.

You’ve already “invested” time and bills into the platform.

This is sunk cost psychology — humans irrationally factor in past investment when making future decisions.

CRED designed this deliberately.

The longer you stay, the more data they collect, and the more valuable you become to their business partners.

What Founders Can Learn From CRED

CRED’s strategy teaches one powerful lesson:

Your initial product doesn’t have to be your real product. It just has to attract the right people.

Think about your own startup or business idea:

- What can you give away that attracts exactly the right audience?

- What does that audience’s attention or data unlock for you later?

- What keeps them coming back once they arrive?

CRED answered all three questions perfectly.

So Why Does CRED Give You Rewards?

Because your bill payment was never the point.

Your data, your attention, and your financial profile — that’s what CRED was always after.

The rewards just made sure you showed up willingly.

That’s not generosity. That’s a business model.

Understanding business means understanding the game behind the game.

Learn business casually — one concept every week.

One Comment